Is There A Limit When Increasing HOA Fees? What’s The Basis?

Increasing HOA fees are a huge pain point for many members of an HOA-run community. But, can an HOA board even legally raise the fees?

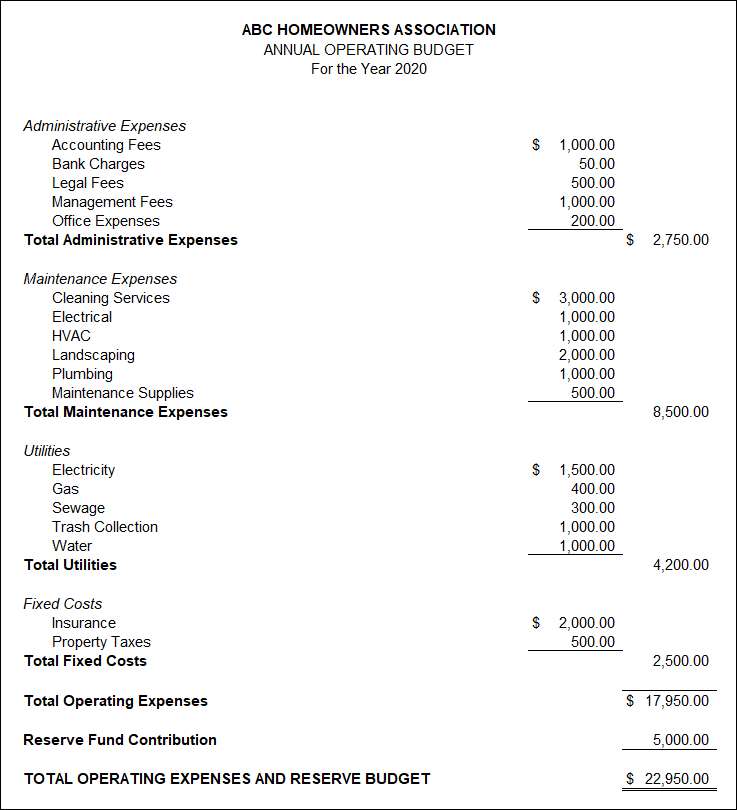

Increasing HOA Fees: It All Starts With Budgeting

To truly grasp the need for fee increases, you must first understand how homeowners associations work. Homeowners associations exist to maintain the community and protect property values. This includes coordinating and paying for various expenses such as landscaping, maintenance, repairs, and the like. And the money used to pay for these expenses comes from the homeowners, who automatically become members of the HOA when they purchase a home in the community.

But, how exactly do HOAs determine how much to charge homeowners?

Every HOA community is run by a set of elected board members who are responsible for creating an annual budget. They do this by anticipating the expenses for the coming year based on historical data and a number of other factors. Once they determine how much the HOA will need for the coming year, they will divide that among the homeowners in the community, including themselves. Whether or not the amount is divided equally or based on a percentage will depend on what your governing documents say.

This is how an HOA board calculates its regular dues or fees.

Why Would an HOA Need to Increase HOA Fees?

The HOA board repeats the process of creating a budget and determining the fees every year. As such, changes will naturally occur. For owners, the idea of increasing homeowners association fees may be unwelcome. But, there are a couple of possible reasons for a dues increase.

1. External Economic Factors

1. External Economic Factors

This refers to factors beyond the HOA’s control, such as inflation, wage increases, and the rising cost of goods. Although your association may not directly utilize labor or materials, your vendors surely do. And, if your vendors hike up their rates as a result, your HOA will certainly follow.

2. Not Enough Reserves

Another reason why your board would need to update HOA fees is to meet the right reserve level. During the budgeting process, your board will need to allocate funds for operating and administrative expenses. A portion of the funds, though, should also go to your reserve fund.

The reserve fund is an account designated for major repairs and replacements in the future or for unexpected costs that arise. Associations must meet a certain percentage in their reserves (obtained through a reserve study) to have what is considered a healthy reserve level. Maintaining the proper reserve level will eliminate the need for special assessments when major replacements or repairs inevitably come up.

If you don’t have well-funded reserves, the need to levy special assessments or increase regular dues will also arise. It just means you will have to charge a significantly higher fee to meet your budget deficit.

Increasing HOA Fees: What Do State Laws Say?

Even though an HOA board can raise dues according to their budgetary needs, they don’t always have unlimited freedom in this aspect. Some states restrict fee increases or limit how much a board can charge on a yearly basis. There are also laws that require boards to obtain approval from the membership if they want to increase fees by a certain percentage.

For instance, according to Section 33-1803 of the Arizona Revised Statutes, homeowners associations are not allowed to raise fees by more than 20 percent per year without getting a majority vote from the membership. Since state laws can vary, though, it is best to check with your legal counsel before taking action.

For board members, it is important to know these limits to avoid potential liability. For homeowners, it is important to know these limits to keep the board in check. But, it is equally vital that owners understand that dues increases are sometimes necessary to keep the community in good condition.

Increasing HOA Fees: What Do Your Governing Documents Say?

Sometimes, state laws remain silent or defer to an association’s governing documents for fee increase regulations. You will usually find such limitations within your CC&Rs, though they are more common in older developments than newer ones. No two HOAs are exactly alike, so the restrictions in one community may differ from yours. More often than not, an association’s CC&Rs will limit increases by a fixed percentage or a dollar amount.

Homeowners may feel relieved to know that their association has such limitations in place. But, when these limitations are too extreme, it can hurt the community in the end. When the board can’t collect the necessary funds because of the restriction, it may not meet the budget. This will force the board to cut corners or eliminate certain expenses altogether. The community and its common areas will then inevitably deteriorate, causing curb appeal to fall and property values to plummet.

How to Avoid Increased HOA Fees

One of the most effective ways to avoid increasing HOA fees is to budget smartly. An HOA board should not allocate more funds than it needs to pay for expenses. No frivolous spending.

One of the most effective ways to avoid increasing HOA fees is to budget smartly. An HOA board should not allocate more funds than it needs to pay for expenses. No frivolous spending.

It also helps to actively look for ways to save money without sacrificing quality. You can do this by investing in energy-efficient systems. Even adopting a simple schedule for sprinklers and making sure to turn off the lights when not in use can save you money in the long run.

Additionally, your HOA board should do its due diligence when picking out vendors. Don’t just go for the first vendor you see — nor is it wise to only go with the cheapest one possible. Send out a request for proposal and examine each candidate closely. Weigh out their fees against the services they offer. You can also try asking for a discount, especially if you have been working with the same vendor for years.

Finally, while it may not seem like it, investing in HOA management software can help you save money, too. HOA software comes equipped with sophisticated accounting and financial management modules that can analyze your spending. This will make it far easier to see where your HOA is overspending.

Part of the Job

Increasing HOA fees are simply a normal part of living in an HOA community. As a board member, it is your job to ensure the proper maintenance of the common areas. If that means having to raise dues, then so be it. You might get some pushback from homeowners, but it is important to clearly explain to them why the increase is necessary. Remind owners what the fees are for and that low fees don’t always benefit the association.

Are you having a hard time with budgeting and calculating fees? Do you need accurate reports that analyze your HOA’s spending? Condo Manager can help with all that and more. Call us today at (800) 626-1267 to learn more about our software or contact us online to get a free demo.

RELATED ARTICLES:

- Your Ultimate Guide to HOA Fees

- What Should An HOA Budget Template Have?

- HOA Vendor Management: Keep Track Of Your Vendors With Ease

Homeowners miss payments all the time for any number of reasons. Sometimes, they don’t have time to write and mail in their checks. Other times, they simply forget. An HOA online payments system, though, can greatly reduce instances of late payments.

Homeowners miss payments all the time for any number of reasons. Sometimes, they don’t have time to write and mail in their checks. Other times, they simply forget. An HOA online payments system, though, can greatly reduce instances of late payments. The entire point of using an electronic payment system is to make it more convenient for everyone. As such, you should consider the users. The system should be easy enough for homeowners to navigate, so much so that they will actively choose to use it over traditional methods.

The entire point of using an electronic payment system is to make it more convenient for everyone. As such, you should consider the users. The system should be easy enough for homeowners to navigate, so much so that they will actively choose to use it over traditional methods.

Some associations offer discounts to owners who pay their dues ahead of time.

Some associations offer discounts to owners who pay their dues ahead of time.

While it is good practice to review past budgets, they can only tell you what happened in previous years. But, things can change over time.

While it is good practice to review past budgets, they can only tell you what happened in previous years. But, things can change over time.

Dues and assessments are the lifeblood of every homeowners association. Without them, an HOA community would suffer detrimental consequences.

Dues and assessments are the lifeblood of every homeowners association. Without them, an HOA community would suffer detrimental consequences. While it is required for some associations to share the total delinquency amount to homeowners, a majority are not allowed to disclose detailed information. In Nevada, for instance, the law

While it is required for some associations to share the total delinquency amount to homeowners, a majority are not allowed to disclose detailed information. In Nevada, for instance, the law

Unfortunately, not all HOA board members have a background in accounting. This makes it difficult to prepare financial reports, including the accounts payable report. While many turn to HOA management companies or accountants for help, another alternative is to invest in software.

Unfortunately, not all HOA board members have a background in accounting. This makes it difficult to prepare financial reports, including the accounts payable report. While many turn to HOA management companies or accountants for help, another alternative is to invest in software.

The general ledger acts as the master copy of all financial transactions in a homeowners association. It contains all accounting data, including those posted from your sub-ledgers and journals. Therefore, an HOA general ledger should include all

The general ledger acts as the master copy of all financial transactions in a homeowners association. It contains all accounting data, including those posted from your sub-ledgers and journals. Therefore, an HOA general ledger should include all  Accrual accounting is the most widely used approach because of its accuracy and reliability. It is also the only accounting method that conforms with the

Accrual accounting is the most widely used approach because of its accuracy and reliability. It is also the only accounting method that conforms with the

Operating Activities. This part consists of cash sourced from and spent on business activities. For an HOA, that could mean

Operating Activities. This part consists of cash sourced from and spent on business activities. For an HOA, that could mean  On paper, the homeowners cash flow statement seems easy to prepare. But, it actually takes a lot of organizing, cross-checking, and discipline to properly put one together. Many companies have teams of accountants and professionals for this kind of task. Homeowners associations, though, typically only have their board to rely on.

On paper, the homeowners cash flow statement seems easy to prepare. But, it actually takes a lot of organizing, cross-checking, and discipline to properly put one together. Many companies have teams of accountants and professionals for this kind of task. Homeowners associations, though, typically only have their board to rely on.

Homeowners associations function in much the same ways as a business. And just like a business, HOAs need financial statements to guide their financial decisions.

Homeowners associations function in much the same ways as a business. And just like a business, HOAs need financial statements to guide their financial decisions. While many associations hire an accountant or a management company to help prepare their financial reports, you can achieve equally great results with management software.

While many associations hire an accountant or a management company to help prepare their financial reports, you can achieve equally great results with management software.